Lender Solutions

UCC, Lien and Litigation Search Services

Let Ficoso take the complexity out of your searches and get you the information

you need when you need it.

Searching made easy with the Ficoso Portal

Search in any jurisdiction from one portal

with timely nationwide data.

Never miss incorrectly filed liens and entities

thanks to wild card search that finds matching names and variations.

Save time and effort with an easy-to-use UI

which enables you to pull up past search results and previously ordered copies quickly.

Get personalized, expert support

for your searching needs from the industry-leading UCC specialists.

Accurate, timely public records searches

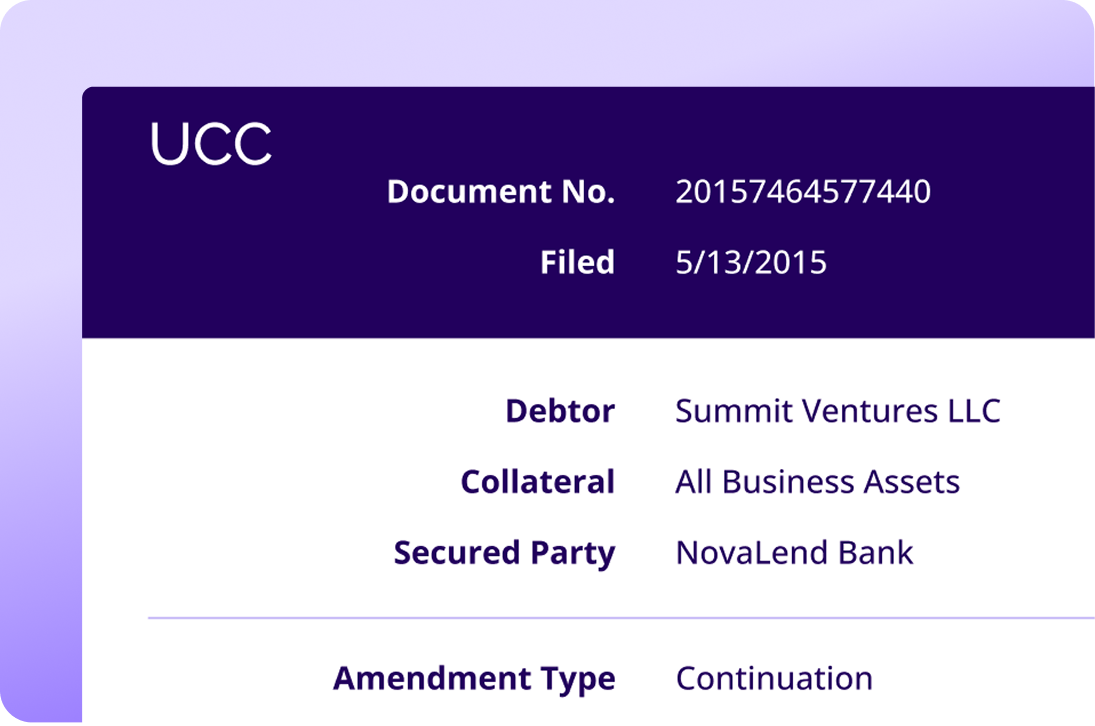

Searching across different jurisdictions for UCC records, liens, and business entity statuses is complex and time-consuming. Our UCC portal simplifies your search and mitigates risks.

- Search online with real-time data sourced directly from all 50 Secretary of State offices.

- Our white glove offline search service covers 3,600+ county and state jurisdictions.

- Access the portal directly from within your own loan origination system with simple API integrations.

- Broad-based name searching ensures you don’t miss any files entered under similar names or name variations.

- Easy-to-read search reports are organized and formatted for optimal clarity.

- Save time by creating UCC filings directly from your search results.

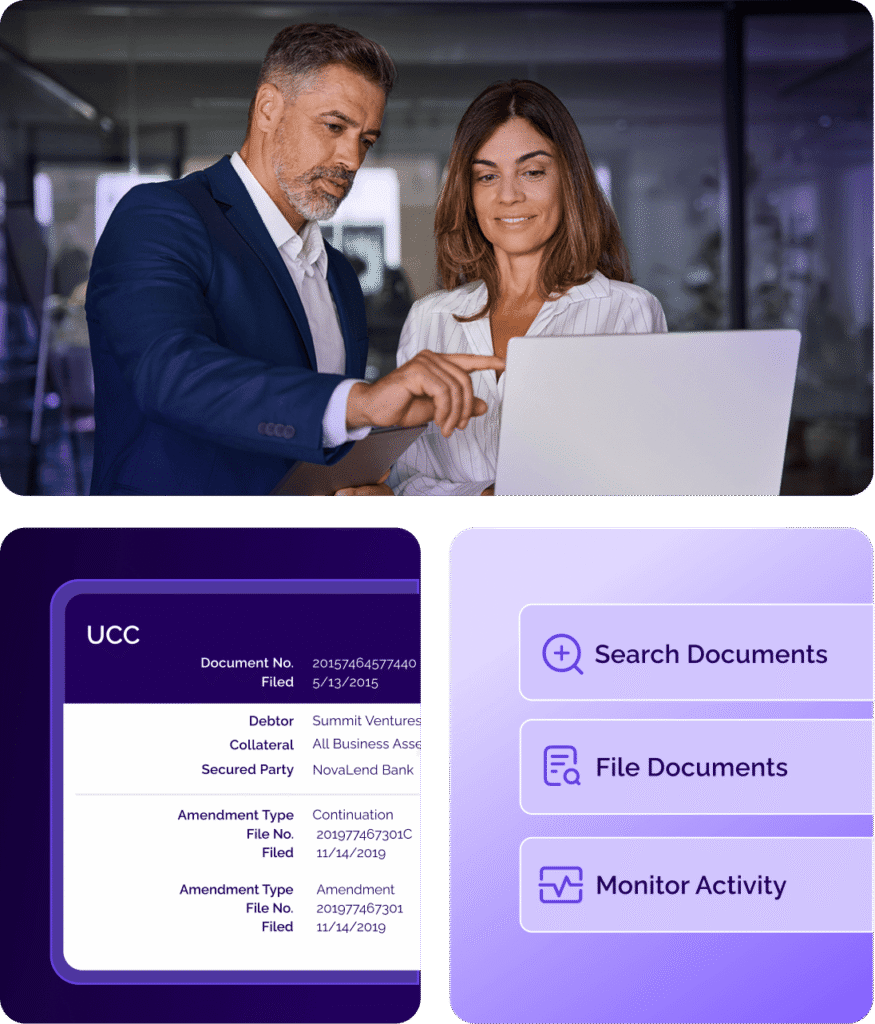

How it works

UCC searches have never been so simple

We do all the hard work for you, so you can accurately search without needing to know how different jurisdictions operate.

Step 1

Access our portal

by logging in through our site or plug Ficoso directly into your LOS system for ease of use.

Step 2

Follow our helpful tool tips

that walk you through the search process.

Step 3

Review simple visual results

organized for clarity and in easy-to-read document images.

Step 4

Create your UCC filing

directly from your search results to save time and avoid input errors.

Litigation Research

The litigation information you need, when you need it

Choose the most accurate, timely and comprehensive litigation search and retrieval services available and discover all the advantages that come with partnering with First Corporate Solutions’ uniquely trained network of dedicated field searchers.

- Search by plantiff, defendant or both for case retrievals in any timeframe.

- Receive detailed reporting of uncovered cases and find party information, case status, and/or the nature of the report

Secured party search reports

Give diligence its due with accurate secured party search reports

- Make lending decisions based on data that’s high-quality, dependable, and easy to use.

- Request a secured party search report from Ficoso to disclose any active UCCs and liens that name a given creditor as a secured party.

- Our timely reports are delivered in a convenient spreadsheet format to give you the flexibility to sort and filter the data as needed.

Expert services

Meet any due diligence challenge with support from the UCC and public records specialists

At Ficoso, we pride ourselves on our top-notch service and support, so you can access the data you need, whether it’s accessible online or not.

- Personalized customer service with a dedicated support specialist

- Experienced and knowledgeable staff who have conducted hundreds of thousands of searches

- Expert correspondents provide accurate and timely offline searches

- Simple and transparent pricing structure ensures you only pay for what you need

Why Ficoso

Get the information you need to make confident lending decisions

Save Effort

We’re dedicated to making our solutions as simple and user-friendly as possible, with integrations that further streamline your processes.

Save Your Sanity

We obsess over the accuracy and timeliness of our data so you don’t have to worry about missed details derailing your deals.

Save the Day

When something goes wrong or you need offline service, we are the expert professionals who truly understand the complexities of public records data.

Our Network

Your access to every state, county, and courthouse jurisdiction in the U.S.

FAQs

Learn more with answers to commonly asked questions.

-

Is there a web UI that shows test data we submit for filings?

Yes, you can verify the data entered is appearing in the right places on the UCC filing documents by visiting the companion website tied to the sandbox data.

-

How many users can I have on my profile?

You can have as many users as you like

-

What options do you have for receiving my monitoring alerts?

Monitoring alerts are both emailed and viewable in the portal. You can also filter to see all alerts within a given date range, and sort, filter, or export that data.

-

How can I begin setting up an API?

Reach out to us or schedule a consultation so we can understand which integration(s) would best suit your needs, and we will provide support and access to our API documentation so you can get started. We have a convenient sandbox environment so that you can fully test it out first.

-

Can we search in all 50 states at once?

Each state holds different indexes so while you can search in all states with Ficoso, it may not be cost effective to search in all states at once.

-

Do State level searches also cover county-level UCCs?

Unfortunately, each state and county only handle their own indexes. However, if you need to complete a more in-depth search at both levels, you can reach out to your Client Services Specialist, who can walk you through your specific situation and find the solution best for you.

Let’s talk about how we can make your life easier

Ready to take the complexity out of UCC and public records due diligence? Just tell us a bit about your needs and we’ll get the ball rolling.